SMM June 17 news:

Metal market:

Domestic base metals showed mixed performance overnight, with SHFE tin slightly down. SHFE copper rose 0.45%. SHFE nickel fell 0.48%. SHFE lead gained 0.35%. SHFE aluminum edged down 0.02%, while SHFE zinc advanced 0.62%. Additionally, the most-traded alumina futures contract increased 0.18%, and the most-traded cast aluminum contract climbed 0.64%.

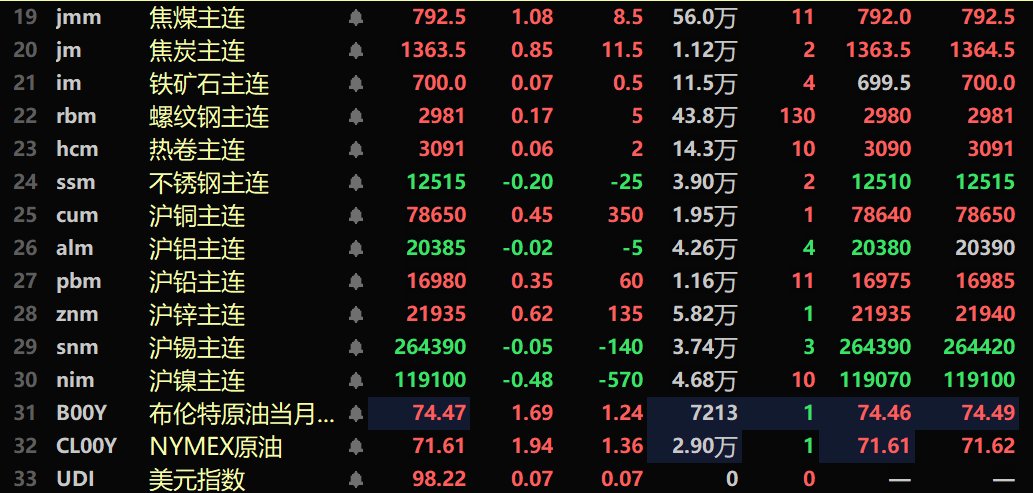

Overnight ferrous metals series mostly rose, with iron ore up 0.07%, stainless steel down 0.2%, rebar gaining 0.17%, and HRC slightly higher. For coking coal and coke: coking coal rose 1.08%, coke increased 0.85%.

Overnight overseas market metals saw LME base metals generally rise, with LME copper up 0.52%, LME aluminum gaining 0.56%, LME lead rising 0.8%, LME zinc jumping 1.41%, while LME tin fell 0.44% and LME nickel declined 0.42%.

Overnight precious metals: COMEX gold dropped 1.4%; COMEX silver edged up 0.04%. SHFE gold fell 1.37%, SHFE silver decreased 0.08%.

As of 8:15 am June 17, overnight closing quotes

》Click to view SMM futures data dashboard

Macro front

Domestic:

[Notice: MOFCOM to hold press conference on 19th regarding key work in commerce sector]The Ministry of Commerce will hold a press conference at 3 pm on Thursday, June 19, 2025, where its spokesperson will introduce recent key work in the commerce sector and take questions from reporters.

[NAFMII convenes symposium on supporting high-quality development of automakers in China's interbank market]NAFMII held a symposium on June 16, 2025, discussing interbank market support for high-quality development of automakers. Representatives from automakers and lead underwriters attended, with the meeting chaired by NAFMII Vice President Zhong Xu. The association presented interbank market support for the automotive industry. Representatives from 9 companies - FAW, SAIC, BAIC Group, BYD, Geely Holding, Great Wall Motor, NIO Group, XPeng Motors, and Xiaomi Group - described challenges faced amid cut-throat competition and proposed suggestions for optimizing financing environment. Lead underwriters conducted on-site matchmaking for automakers' financing needs. Next, NAFMII will implement the Party Central Committee and State Council's strategic deployment on developing new quality productive forces through technological innovation, strengthen bond market system building and product innovation, optimize financial services tailored for the automotive sector, encourage automakers to increase bond financing while maintaining healthy development and avoiding disorderly competition, and actively promote intelligent, high-end, green transformation to advance China's automotive industry toward high-quality development. Cailian Press)

[CPCA: 52,000 Pickup Trucks Sold in May, Up 13.6% YoY] According to data from the China Passenger Car Association (CPCA), in May 2025, 51,700 pickup trucks were produced nationwide, up 20.8% compared to May 2024. From January to May 2025, 255,000 pickup trucks were produced, up 23.4% YoY. In May 2025, 52,000 pickup trucks were sold in the market, up 13.6% compared to May 2024, and down 8.1% MoM from the previous month, remaining at a high level in the past five years. From January to May 2025, 258,000 pickup trucks were sold, up 18.2% YoY compared to January-May 2024.

[Goldman Sachs Bullish Again: Global Capital Returns to China, Optimistic About China's "Top 10" Stocks] Kinger Lau, Chief China Equity Strategist at Goldman Sachs, recently released a research report titled "The Return of China's Private Enterprises: The Tide Has Turned." Lau pointed out that driven by various macro, policy, and micro factors, the medium-term investment prospects for China's private enterprises are improving. Goldman Sachs has listed China's "Top 10," namely the ten Chinese private publicly listed firms that Goldman Sachs is particularly bullish on. They are: Tencent, Alibaba, Xiaomi, BYD, Meituan, NetEase, Midea, Hengrui Medicine, Ctrip, and Anta. 》Click for details

US Dollar:

The US dollar index rose 0.03% overnight, closing at 98.15. The market is focused on the tense situation between Israel and Iran, as well as the US Fed's policy meeting this week. The Fed meeting will conclude on Wednesday. The market generally expects the Fed to keep interest rates unchanged. However, the market will be watching how the Fed views recent data, which generally indicate softening economic activity, but the risk of rising price pressures remains high.

Other Currencies:

Leaders of the Group of Seven (G7) began their annual summit in Canada. With about three weeks left until Trump's deadline for trade agreements, the market remains nervous as agreements with major trading partners such as the EU and Japan have not yet been signed. They will be looking for any progress made in any bilateral talks with the US on the sidelines of the G7 leaders' summit. (Webstock Inc.)

Data:

Today, data such as the Bank of Japan's policy benchmark interest rate on June 17, the ZEW Economic Sentiment Index for the Eurozone in June, the ZEW Economic Sentiment Index for Germany in June, the US monthly import price index for May, the US annual import price index for May, the US monthly retail sales for May, the US monthly core retail sales for May, the US annual retail sales for May, the US monthly retail sales control group associated with GDP for May - seasonally adjusted, the US monthly industrial output for May, the US capacity utilization rate for May, the US monthly manufacturing output for May, the US manufacturing capacity utilization rate for May, and the US annual industrial output for May - seasonally adjusted, will be released. In addition, it is worth noting that: Today, 182 billion yuan of one-year medium-term lending facility (MLF) matured; Bank of Japan Governor Kazuo Ueda held a monetary policy press conference; the Bank of Japan announced its interest rate decision; US President Trump visited Canada from June 15 to 17 to attend the G7 Leaders' Summit.

Crude oil:

Both WTI and Brent crude oil futures fell, with WTI down 2.06% and Brent down 2.33%. Market concerns about disruptions to crude oil supplies in the Middle East eased, leading to a decline in oil prices.

The US Navy said on Monday that electronic interference with commercial shipping navigation systems around the Strait of Hormuz had surged in recent days, affecting vessels passing through the area. Approximately one-fifth of global oil consumption, or about 18-19 million barrels per day (bpd) of oil, condensate, and fuels, passes through the Strait. Iran, a member of the Organization of the Petroleum Exporting Countries (OPEC), currently produces about 3.3 million bpd of oil and fuels and exports more than 2 million bpd. Analysts and OPEC observers said that the spare capacity of OPEC oil-producing countries to increase production to offset any disruptions is roughly equivalent to Iran's production.

A preliminary survey showed that US crude oil and distillate inventories likely fell last week, while gasoline inventories may have increased. Before the weekly inventory report was released, the average forecast of four surveyed analysts was that US crude oil inventories increased by about 600,000 barrels in the week ending June 13. US distillate inventories, including diesel and heating oil, were expected to decrease by about 100,000 barrels, while gasoline inventories were expected to increase by 200,000 barrels. The American Petroleum Institute (API) will release its weekly crude oil inventory report at 4:30 AM Beijing time on Wednesday, and the US Energy Information Administration (EIA) will release its weekly crude oil inventory report at 10:30 PM Beijing time on Wednesday. (Webstock Inc.)